The Coverage Illusion: Every Front Door to Your Health System Needs a Self-Pay Strategy — and Employers Are Already Building Their Own

As deductibles hit historic highs and Medicaid coverage erodes, insured patients are functionally uninsured for most of the year. Every access point in your care model — urgent care, primary care, employer clinics — must now price and package services for a patient who pays like a consumer, not a beneficiary.

The commercial patients arriving at your front door in 2026 are carrying insurance cards that, for much of the year, don't function like insurance. And a patient who defers care today becomes a higher-acuity, higher-cost patient tomorrow — in your ED, on your books.

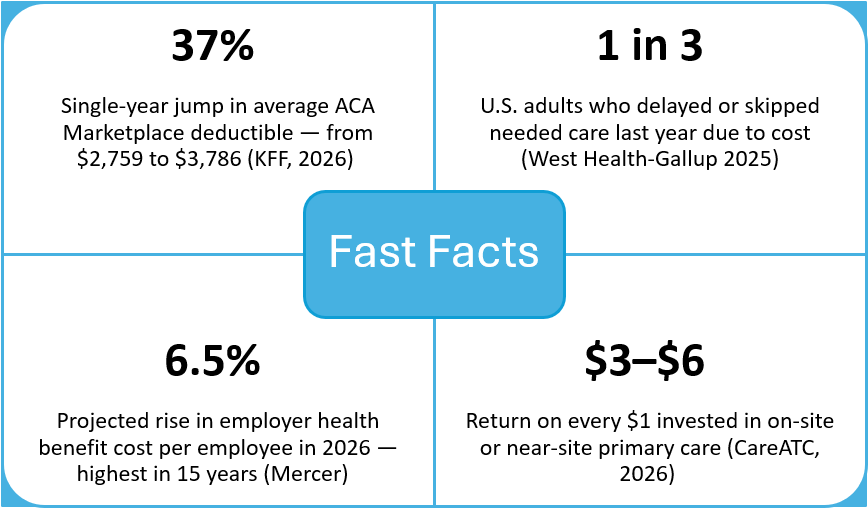

The average ACA Marketplace deductible jumped 37% in a single year to $3,786 in 2026 — the steepest increase in Marketplace history. Bronze plan enrollment, where deductibles average $7,476, surged from 30% to 40% of all selections. For millions who lost Medicaid under the One Big Beautiful Bill's restructuring, there is no coverage at all. Every front door your organization operates is now serving patients who think and spend like consumers. The question is whether your pricing model reflects that.

Urgent care gets the most attention because the price gap versus the ED is obvious to any patient with a smartphone. But every clinical front door is exposed because the same financial pressure falls on other entry points like primary care. Pre-deductible High-Deductible Health Plan (HDHP) patients face $143 to $330 or more for a non-well primary care visit — before labs or imaging. That cost deters the longitudinal, preventive care that keeps chronic conditions manageable. Research in JAMA Network Open links HDHP enrollment to significantly reduced evidence-based care use across asthma, diabetes, hypertension, heart failure, and depression. Those are not deferred elective visits. They are the exacerbations filling up your ED six months later.

The HDHP patient is insured in name but is often Self-Pay in practice. Average single-coverage deductibles hit $1,886 in 2025; workers at small firms averaged $2,631. Employers aren't reversing course — 59% planned to raise deductibles or cost-sharing in 2026, up from 48% the year before. The predictable result: patients deferring care, accumulating disease burden, and arriving at your access points with more complexity and less ability to pay.

47% of U.S. adults are worried they won't be able to afford healthcare in 2026 — the highest level ever recorded. Deferred care doesn't disappear. It becomes a chronic disease burden, delayed diagnosis, and higher acuity encounters that land on your system in more expensive settings.

If a cost-sensitive patient can't determine what care costs before they decide to seek it, they will either avoid it or go to a competitor who made pricing legible. Transparency is not just a No Surprises Act compliance requirement — it is a patient acquisition tool.

Publish flat-rate self-pay bundles that group the exam, diagnostics, and procedural services for your most common visit types at a single price. Competing against telehealth at $50–$100 and FQHCs on sliding scale, opacity is a disqualifier. Critically, pre-deductible HDHP patients often pay less with the self-pay bundle than running their claim through insurance — and front-desk teams trained to offer that comparison in real time to build loyalty, not just transactions.

The direct primary care (DPC) model — a flat monthly fee of $50 to $179 for unlimited access, no copays, no deductible exposure — is growing fast precisely because it solves the HDHP affordability problem. Health systems not evaluating DPC-adjacent structures are ceding this patient segment to independent practices and retail competitors. At minimum: publish transparent self-pay visit tiers online and at the point of scheduling. A patient who can see a $100–$143 visit price makes a different decision than one facing an opaque billing process.

Employer healthcare costs are projected to rise 6.5%–10% in 2026, the highest in 15 years. Premiums now consume roughly 30% of a family's budget. Employees on HDHPs are deferring care, arriving sicker, missing work, and driving downstream claims. Only 63% of hourly workers say they can afford the care their families need without financial hardship.

The employer-based clinic is the structural response for employers. For every dollar invested in on-site or near-site primary care, employers see $3–$6 in return through reduced claims, lower absenteeism, and productivity gains. With the average primary care wait now at 31 days, an employer clinic eliminates access friction and delivers care at a cost below what employees pay pre-deductible in the traditional insurance model.

The Employer's Problem in 2026

Rising costs, diminishing returns on plan design

Healthcare costs rising 6.5%–10% — highest in 15 years

Employee premium deductions up 6%–7% — effectively a pay cut

HDHP deferrals producing more complex, higher-acuity presentations

Only 63% of hourly workers can afford needed care without hardship

Benefits now the #1 driver of employee retention decisions

Employers are not waiting for health systems and medical groups to implement self-pay strategies. They are already building relationships with DPC networks, occupational health vendors, and benefit consultants. Health systems that don't position themselves as credible employer clinic partners will watch this patient population — and its revenue — migrate to whoever does.

On-site clinics that provide significant medical benefits at no or reduced cost can disqualify employees from HSA participation under IRS guidance. Compatible designs limit services to preventive care and first aid, charge fair market value applied toward the HDHP deductible, or restrict free access to employees who have already met their deductible. Notably, the One Big Beautiful Bill Act clarified that certain DPC arrangements no longer disqualify HSA participation — making DPC-employer partnerships more viable than before. Get the design right at the start; fixing it later is far more disruptive.

The Vantage Perspective

Your pricing model is a care access decision. Treat it like one.

At Vantage Clinical Partners (VCP), our Discovery & Planning work surfaces the same gaps repeatedly: urgent care self-pay tiers not reviewed in years, primary care practices with no published cash-pay pricing, and employer relationships that are transactional rather than strategic. Closing that gap requires operational architecture. It means benchmarking your pricing against local market competitors, designing bundle structures that reflect your actual service mix, and building employer outreach and contracting capability before the competition does. That is the Implementation and Sustainment work we do alongside health system and medical group leaders.

The patient at your front door in 2026 is making a financial decision before they make a clinical one.

For another VCP take on employer-based clinics visit Rising Healthcare Costs Present A Looming Crisis to U.S. Employers .

Beth Papetti, MBA FHM

Principal & Chief Operating Officer

References

Association of Health Care Journalists. (2026, May). How high-deductible health plans can harm patients' health. https://healthjournalism.org/blog/2026/05/how-high-deductible-health-plans-can-harm-patients-health

Business Group on Health. (2025, August 19). 2026 employer health care strategy survey: Executive summary. https://www.businessgrouphealth.org/resources/2026-employer-health-care-strategy-survey-executive-summary

CareATC. (2026, April 14). Why on-site primary care is the foundation of high-performing employers. https://www.careatc.com/blog/why-on-site-primary-care-is-the-foundation-of-high-performing-employers

Direct Primary Care Associates. (2025, March 21). Transforming employee healthcare: Onsite primary care for enterprise businesses. https://directprimarycareassociates.com/2025/03/21/transforming-employee-healthcare-onsite-primary-care-for-enterprise-businesses/

Healthcare Financial Management Association. (2025, May 28). Employers anticipate 2026 to see biggest healthcare cost increase in over a decade. https://www.hfma.org/fast-finance/employers-anticipate-2026-to-see-biggest-healthcare-cost-increase-in-over-a-decade/

Healthcare Financial Management Association. (2026). ACA marketplace final rule could add to payer-mix concerns for providers. https://www.hfma.org/payment-reimbursement-and-managed-care/aca-marketplace-final-rule-provider-payer-mix/

Healthgram. (2018). Near-site or onsite clinics: How to choose the best model for your business. https://www.healthgram.com/insights/near-site-or-onsite-health-clinics-how-to-choose-the-best-fit/

KFF. (2025). 2025 employer health benefits survey. https://www.kff.org/health-costs/2025-employer-health-benefits-survey/

KFF. (2026). The average Marketplace deductible grew by about $1,000 per person in 2026, with more enrollees shifting to higher-deductible plans as enhanced tax credits expired. https://www.kff.org/affordable-care-act/the-average-marketplace-deductible-grew

KFF. (2026, April 30). Americans' challenges with health care costs. https://www.kff.org/health-costs/americans-challenges-with-health-care-costs/

KFF. (2026, March 30). Cost concerns and coverage changes: A follow-up survey of ACA Marketplace enrollees. https://www.kff.org/public-opinion/a-follow-up-survey-of-aca-marketplace-enrollees/

Mercer. (2025). 2025 national survey of employer-sponsored health plans: Employers prepare for the highest health benefit cost increase in 15 years. https://www.mercer.com/en-us/insights/us-health-news/employers-prepare-for-the-highest-health-benefit-cost-increase-in-15-years/

NBC News. (2025, November 19). Gallup poll: A record number of U.S. adults are anxious about health costs going into 2026. https://www.nbcnews.com/health/health-news/gallup-poll-record-number-adults-anxious-health-costs-2026-rcna244358

RSM US. (2026, February 6). IRS Notice 2026-5: Expanded HDHP definition in OBBBA broadens access to HSAs. https://rsmus.com/insights/services/business-tax/irs-notice-2026-expanded-hdhp-definition-obbba-broadens-hsa.html

SHRM. (2025, September 16). Employers brace for 15-year-high health benefit cost hike. https://www.shrm.org/topics-tools/news/benefits-compensation/employers-brace-15-year-high-health-benefit-cost-hike

StemWave. (2025, December 10). Why 2026 will be the year for cash-based medicine. https://stemwave.com/blog/2026-cash-pay-medicine/